- Stats: 1533 0

- Author: Money Bloggess

- Posted: February 7, 2019

- Category: Mortgages

Canada’s Housing Market Update

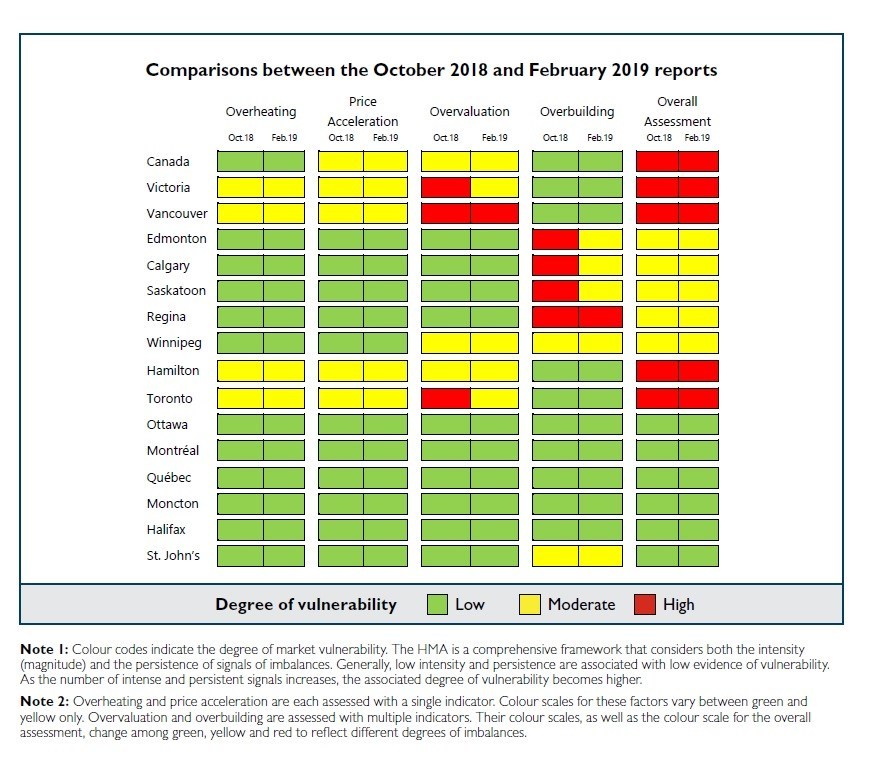

While overvaluation has eased in Toronto and Victoria, Canada’s overall housing market remains vulnerable for the tenth quarter in a row, according to the most recent Housing Market Assessment (HMA) released by Canada Mortgage and Housing Corporation (CMHC).

On a quarterly basis, CMHC issues the HMA to provide Canadians with expert and impartial insight and analysis, based on the best data available in Canada. This report provides a comprehensive view of housing market vulnerabilities and identifies imbalances. It does not identify long-term fundamental affordability challenges.

Results are based on data as of the end of September 2018; the annual rental apartment vacancy rates are from October 2018 and market intelligence as of the end of December 2018. This national report provides the housing market assessment at the national level and summary assessment results for 15 Census Metropolitan Areas (CMAs). For each of these CMAs, CMHC also issues a local report with more information and analysis.

Key Highlights:

- Despite improved alignment between house prices and housing market fundamentals in the previous quarter, moderate evidence of overvaluation continued to be detected for Canada as a whole in the third quarter of 2018.

- The degree of overall vulnerability remains high for Vancouver, Victoria, Toronto and Hamilton. Overvaluation is still detected in all these centres but it is easing as house prices are moving closer to levels supported by housing market fundamentals such as population, personal disposable income, and interest rates. As a result, the evidence of overvaluation has changed from high to moderate in Toronto and Victoria.

- While imbalances in Metro Vancouver‘s housing market have eased in recent quarters, home price levels are high relative to local economic fundamentals, leading to CMHC’s continued detection of overvaluation.

- In Hamilton, overheating and price acceleration continue to be signaled. Despite conditions of overvaluation easing over the past few quarters, moderate evidence of overvaluation is still detected. With the inventory of completed and unsold new homes decreasing, evidence of overbuilding remains low. Housing demand is driven by population growth for the 25 to 34 age group, as it remains strong due to high immigration levels, as well as high in-migration from the GTA.

- Both Calgary and Edmonton continued to show a moderate degree of overall vulnerability in the third quarter of 2018. However, as the rental apartment vacancy rates declined, the evidence of overbuilding has eased from high to moderate in these two centres.

- Saskatoon, Regina and Winnipeg all continued to show a moderate degree of overall vulnerability in their respective markets. In Saskatoon, the inventory of completed and unsold units has stayed below CMHC’s threshold over the past three quarters. Therefore, evidence of overbuilding has changed from high to moderate. In Regina, evidence of overbuilding remained high due to a high vacancy rate and elevated new housing inventory. Winnipeg continues to see a moderate degree of overvaluation and overbuilding, and the overall assessment of the housing market is unchanged from the previous quarter.

- A low degree of overall vulnerability is sustained for Ottawa, Montréal, Québec City, Moncton, Halifax and St. John’s. The resale market in Montréal continues to be closely monitored as a result of a tightening between supply and demand, creating significant upward pressure on house prices.

Related Posts