- Stats: 4791 0

- Author: Linda

- Posted: September 23, 2019

- Category: Fraud and Scams, Insurance, Insurance Bureau of Canada

How to avoid insurance fraud

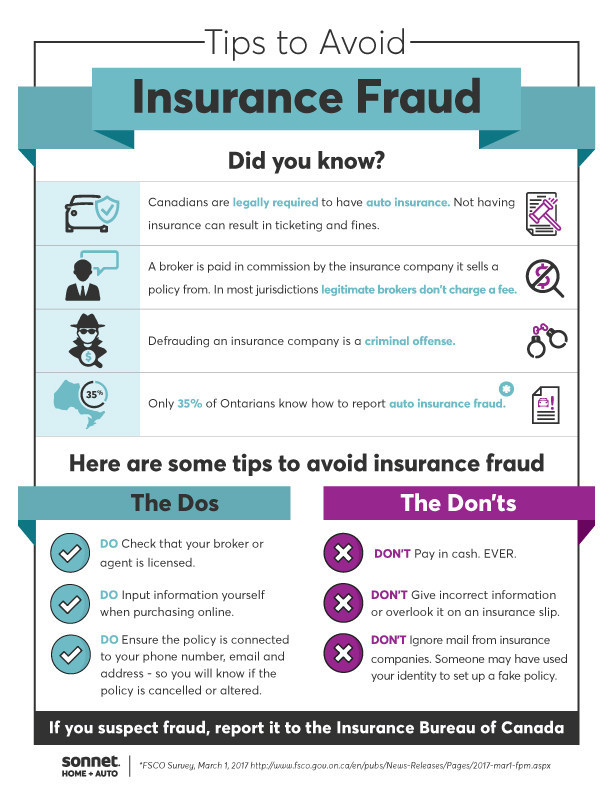

Sonnet Insurance wants to empower Canadians to recognize and prevent potentially harmful scams. Home and auto insurance seller fraud is common in all regions of Canada, especially the GTA1, where victims who don’t understand the process for purchasing home and auto insurance are targeted.

Seller fraud takes place when insurance policies are being sold to customers by fraudulent actors. Unlike claims fraud (using fake accidents or reports to cash in on real insurance policies), seller fraud leaves its victims open to a high degree of personal risk. A fraudster will offer discounted insurance and take the victims’ money in return for home and auto insurance pink slips that are invalid or forged.

Legitimate insurance policies are sold in Canada through registered brokers, licensed insurance agents, and regulated direct-to-consumer insurance companies:

- A legitimate broker or agent is an individual or firm that sells insurance policies to clients and has a license number from their provincial regulator

- Direct-to-consumer insurance companies (like Sonnet) are federally regulated and licensed to sell insurance policies directly to the end customer

Sonnet is doing everything possible to protect consumers against fraud – from plain language policy documents to simplifying the online insurance experience – and wants to educate the public on how to identify scams. A few key indicators can help tip off potential victims of insurance fraud, saving them from losing thousands of dollars and failing to have proper insurance coverage in place when it counts. Two of the most common seller scams in Canada are ‘ghost brokers’ and ‘fake brokers’.

Ghost Brokers take money for insurance upfront, provide a pink slip showing proof of insurance then disappear, or ‘ghost’ the customer. Sometimes the slip is simply a forgery. Other times the fraudster will set up an actual policy, download the slip and give it to the victim, then cancel the policy without the knowledge of the victim. What this scam looks like:

A new Canadian sees an ad for cheap insurance rates online and agrees to meet the ghost broker in a coffee shop with cash to pay a full year’s premiums. The ghost broker exchanges the cash for an insurance slip and pockets the money. The victim thinks the coverage is real until an inspection or accident prompts a check – and the insurance policy, along with the ghost broker, can’t be found.

Fake Brokers have an actual physical address and may do some legitimate business, such as selling or financing cars. Fake brokers purchase an insurance policy with the name of the client to secure an insurance slip. However, the policy will include incorrect information such as unlisted high-risk drivers or the wrong address, to obtain more favourable rates. Policies can be cancelled and claims can be denied if information is misrepresented, which makes it hard for the consumer to get insurance coverage in the future. Some fake brokers make money by charging a ‘broker fee’, while others are trying to clear the path to sell a car. In contrast, a certified broker makes a commission from insurance companies and never charges consumers directly for services. What this scam looks like:

An individual with a bad driving record has been quoted a high premium and sees an ad offering cheap insurance to high-risk drivers. The driver visits the fake broker and pays a lower premium to the fake broker in return for an auto insurance slip. The driver gets into another accident and discovers that the insurance policy contains misrepresented information and their policy is cancelled or claims won’t be paid out. After paying for damages out of pocket, the driver is unable to get standard insurance and opts to give up driving.

“In Canada, auto insurance is mandatory and highly regulated by the government,” added Dunbar. “Generally, if a deal looks too good to be true, it probably is. That is because insurance rates are based on pooled risk – companies need to collect enough money to pay out claims in a given year.”

Victims are encouraged to report fraudulent activity. Reporting fraud helps stop repeat offenders and reduces insurance premiums for everyone. To report fraud, visit the Insurance Bureau of Canada website here: report fraud.

Regulatory bodies issue regular warning notices about suspected fraudsters and offer additional resources. Trusted websites are the best place to check on licenses and suspicious activity. Find your provincial regulator here: insurance regulators.

Canadians looking to better understand home and auto insurance can view answers to frequently asked questions at sonnet.ca/FAQs.

1 FSCO Survey, March 1, 2017 http://www.fsco.gov.on.ca/en/pubs/News-Releases/Pages/2017-mar1-fpm.aspx

Related Posts