- Stats: 3892 0

- Author: Money Bloggess

- Posted: August 22, 2018

- Category: CIBC, Seniors

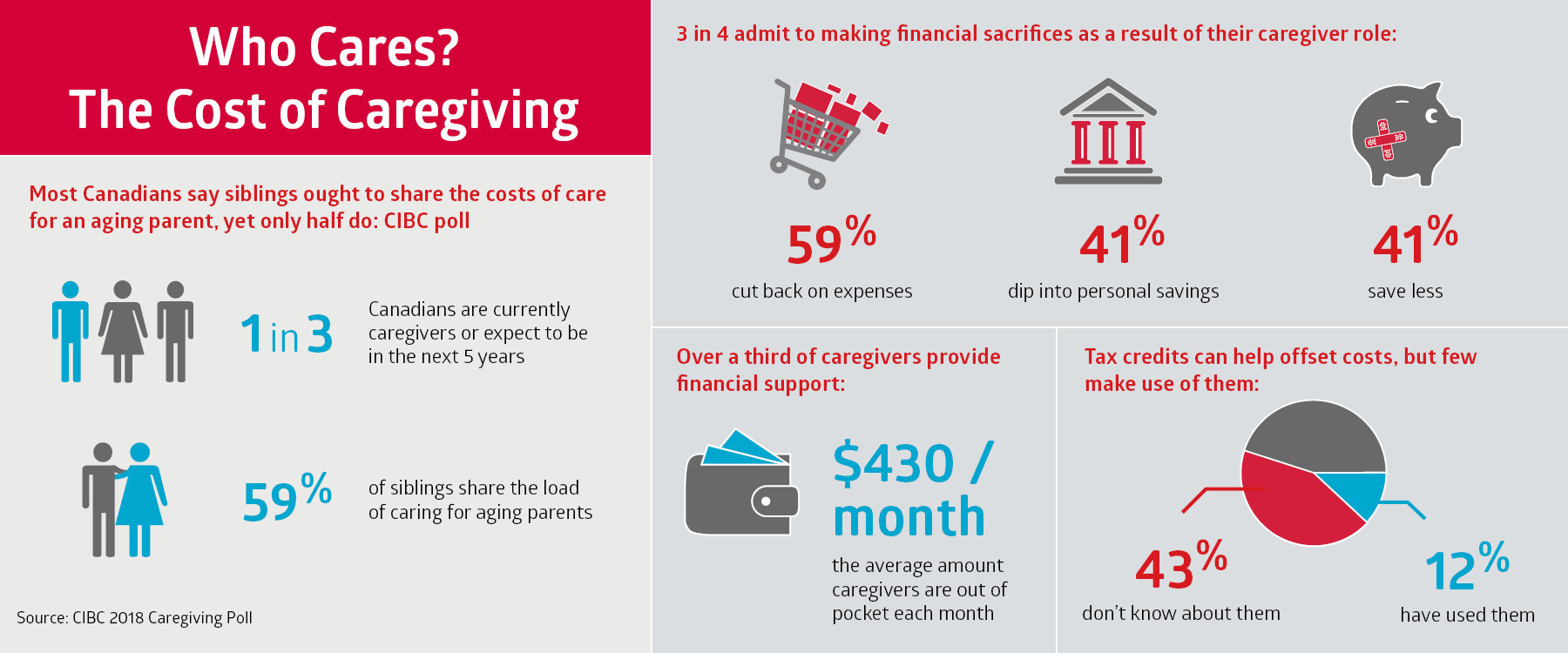

Who Cares? Most Canadians say siblings ought to share the costs of care for an aging parent, yet only half do: CIBC pol

Canadians who financially contribute to the care of a loved one due to advanced age or illness are out of pocket $430 per month on average – an expense many aren’t planning for, finds a new CIBC poll. While most say siblings ought to share the load when caring for an aging parent, only half do (59 per cent), which often leads to family squabbles over how the work and costs should be shared.

Further, while tax credits are available to help ease the financial burden for caregivers, two in five (43 per cent) don’t know about them, and even fewer have used them (12 per cent).

“Providing care for someone you love can be a rewarding experience, but it can be costly and lead to family disputes about how the work and costs should be shared,” says Jamie Golombek, Managing Director, Tax & Estate Planning, CIBC Financial Planning and Advice. “The best way to support a loved one is to plan ahead and discuss arrangements well before any care is needed. Planning for expenses and knowing what funding and tax relief is available can help everyone feel better prepared for the care years ahead.”

The poll found that one-third (33 per cent) of Canadians either currently provide caregiving support or expect to in the next five years – jumping to 40 per cent among those aged 45-55 – with most providing care for an aging parent (44 per cent).

Three-quarters (76 per cent) of caregivers who provide financial support admit they’re making financial sacrifices as a result of their caregiving responsibilities including cutting back on expenses (59 per cent), dipping into personal savings (41 per cent) and saving less (41 per cent).

When it comes to mom or dad, sharing is caring

With the costs of caring for aging parents pegged at $33 billion each year in direct and indirect costs, ranging from parking fees to time off for medical appointments, it’s no surprise that many siblings would opt to share the load when it comes to care for mom or dad.

“The good news is that you may be able to take advantage of some tax credits to lessen the financial burden, even if you’re sharing the costs, ” says Mr. Golombek in a new report entitled, Who Cares? Easing the financial burden for caregivers, which was co-authored with Debbie Pearl-Weinberg, Executive Director, Tax & Estate Planning, CIBC Financial Planning and Advice.

For example, if a parent requires full-time care from a personal support worker and you choose to split the bill with your parent or siblings, then you may each be able to claim the Medical Expense Tax Credit (METC) for these costs. You may each also be eligible for a 15 per cent non-refundable Canada Caregiver Credit up to a shared maximum of $6,986, adds Mr. Golombek.

In addition, the Home Accessibility Tax Credit may provide up to a $1,500 credit for renovations and other one-time expenses, and the Disability Tax Credit (DTC) may provide tax savings of $1,235 federally, plus provincial or territorial tax savings, for individuals with a disability or those who care for them.

The poll also found that in the event that one sibling does bear the lion’s share of hands-on care for an aging parent, two-thirds of respondents (65 per cent) agree that he/she should be financially compensated in some way – either through financial contributions during care or given more than others when the estate is distributed.

“When arrangements are informal, misunderstandings can arise,” says Mr. Golombek. “Having clear conversations and the right paperwork in place, including Powers of Attorney (POA) and a will, an estate plan can help mitigate family disputes and ensure that all assets are managed and divvied up according to mom’s or dad’s wishes.”

Despite the costs, the poll showed that most caregivers (74 per cent) feel grateful for the opportunity to help, and more than half (53 per cent) would do so, even if it put their own financial future at risk.

“Don’t let caregiving be the blind spot in your financial plan. In addition to any out-of-pocket expenses, consider how providing care could impact your own retirement plans if you or your partner had to reduce time at work or even retire earlier than planned to provide full-time care for an aging relative,” he adds. “Having a clear plan in place can help ensure your own financial priorities don’t get sidelined,” he says.

Tips for aging parents to help make the caring years easier for your loved ones:

- Have ‘the talk’ – Talking openly about care needs can be difficult and emotionally charged, but it can also be reassuring, particularly if you talk about it well before you need the care. This CIBC Family Playbook can help guide you through the discussion.

- Set up a trusted network and empower them – Determine who will manage your finances, and healthcare decisions. Discuss your wishes with your lawyer and family members early on so they may ask questions or raise issues you may not have considered. While putting assets into joint ownership might seem like the simplest approach to having someone manage your finances when you’re no longer able to, a better plan would be to have a POA in place.

- Anticipate any costs and budget for plan B – Speak to your financial advisor about your advanced care plan and how you will finance it. If you expect an adult child to become your caregiver or contribute to the costs of care either directly or by providing full-time support, be sure to invite him or her into the conversation to help address any questions and enable them to act on your behalf.

Key poll findings:

- One-third (33 per cent) of Canadians either currently provide caregiving support or expect to in the next 5 years – jumping to 40 per cent among those aged 45-55

- Care for an aging parent is the most common among caregivers (44 per cent)

- Over a third (36 per cent) of current caregivers make financial contributions of about $430 per month on average

- 76 per cent admit they’re making financial sacrifices as a result of their caregiving responsibilities including cutting back on expenses (59 per cent), dipping into personal savings (41 per cent) and saving less (41 per cent)

- 75 per cent of those who don’t yet provide care, but expect to in five years, have taken no steps to prepare

About the CIBC Caregiver Poll: From July 18 to July 20 2018 an online survey of 3025 randomly selected Canadian adults who are members of Maru/Blue’s online panel Maru Voice Canada. For comparison purposes, a probability sample of this size has an estimated margin of error (which measures sampling variability) of +/- 2.5%, 19 times out of 20. The results have been weighted by education, age, gender and region (and in Quebec, language) to match the population, according to Census data. This is to ensure the sample is representative of the entire adult population of Canada. Discrepancies in or between totals are due to rounding.

About CIBC

CIBC is a leading Canadian-based global financial institution with 11 million personal banking, business, public sector and institutional clients. Across Personal and Small Business Banking, Commercial Banking and Wealth Management, and Capital Markets businesses, CIBC offers a full range of advice, solutions and services through its leading digital banking network, and locations across Canada, in the United States and around the world. Ongoing news releases and more information about CIBC can be found at www.cibc.com/en/about-cibc/media-centre.html or by following on LinkedIn (www.linkedin.com/company/cibc), Twitter @CIBC, Facebook (www.facebook.com/CIBC) and Instagram @CIBCNow.

SOURCE CIBC – Consumer Research and Advice

Related Posts